You can invest up to £200,000 per year and get your income taxed reduced by up to £60,000.

This applies to all income that is subject to income tax, including salary, dividends and tax on savings interest.

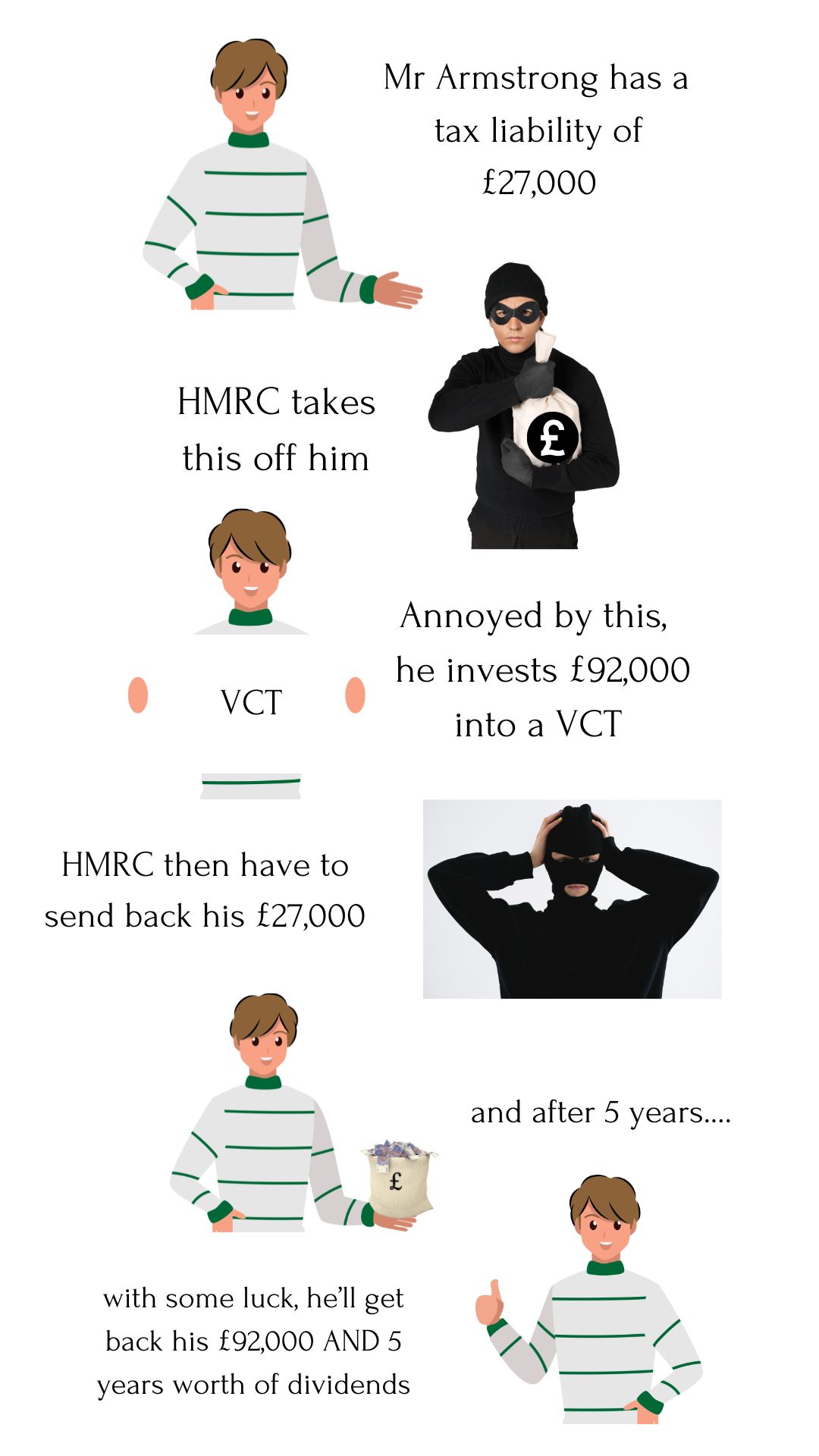

How does a VCT work for an employed person?

Mr Armstrong is employed and earns £110,000 per year. He only pays £10,000 per year into a pension so he has a £100,000 of is income that is taxable.

His income tax liability on the £100,000 works out at £27,428.

He pays £91,426 into a VCT and gets tax relief of 30%, which amounts to £27,428.

In this example, he has completely avoided paying income tax for the year by making this one contribution.

But even if he didn’t want to “wipe out” all of his tax, he could have put a smaller amount into a VCT – a £30,000 investment would have taken off £10,000 of his tax liability.

PLUS, at the end of 5 years, he’ll be able to get back his £91,426 tax free, as well as tax free dividends!

Contact ustoday to find out more about how a VCT can work for you.

If you want advice on how to reduce your tax, or have a question, or just want to have a chat about reducing you tax liability with a UK Qualified Independent Financial Adviser, then phone now on 01793 686393 orcontact usonline.