If you have a pension fund and are over 55, and want to take money out of it without paying income tax, then it is possible to do so using a VCT.

Here’s an example:

Mr Brown, is 55 and has a pension worth £1,000,000.

He wants to use £200,000 of his pension then to buy a holiday home when he retires at 62.

He does not want to pay more money into his pension as he is worried about the lifetime allowance, but does not want to take out all of his tax-free cash either.

He also has substantial savings too.

Here’s how £100,000 could come out of his pension, with no tax to pay…

Here’s what he can do:

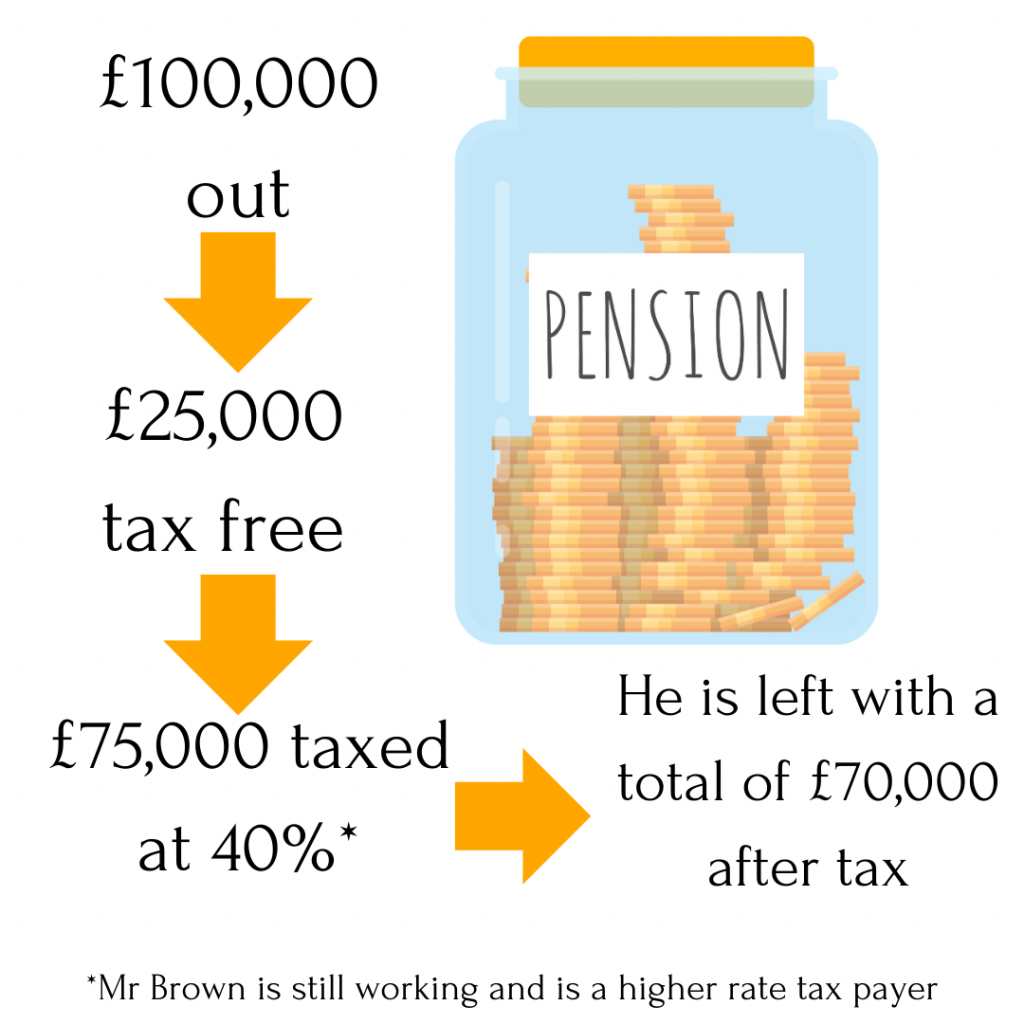

He takes out £100,000 out of his pension.

This is made up of £25,000 tax-free cash, and £75,000 taxable income.

For him this £75,000 is taxed at the higher rate of 40%. This would mean that he pays £30,000 of income tax.

So, after income tax he ends up with £70,000 (£75,000 minus £30,000 tax PLUS his 25% tax free amount).

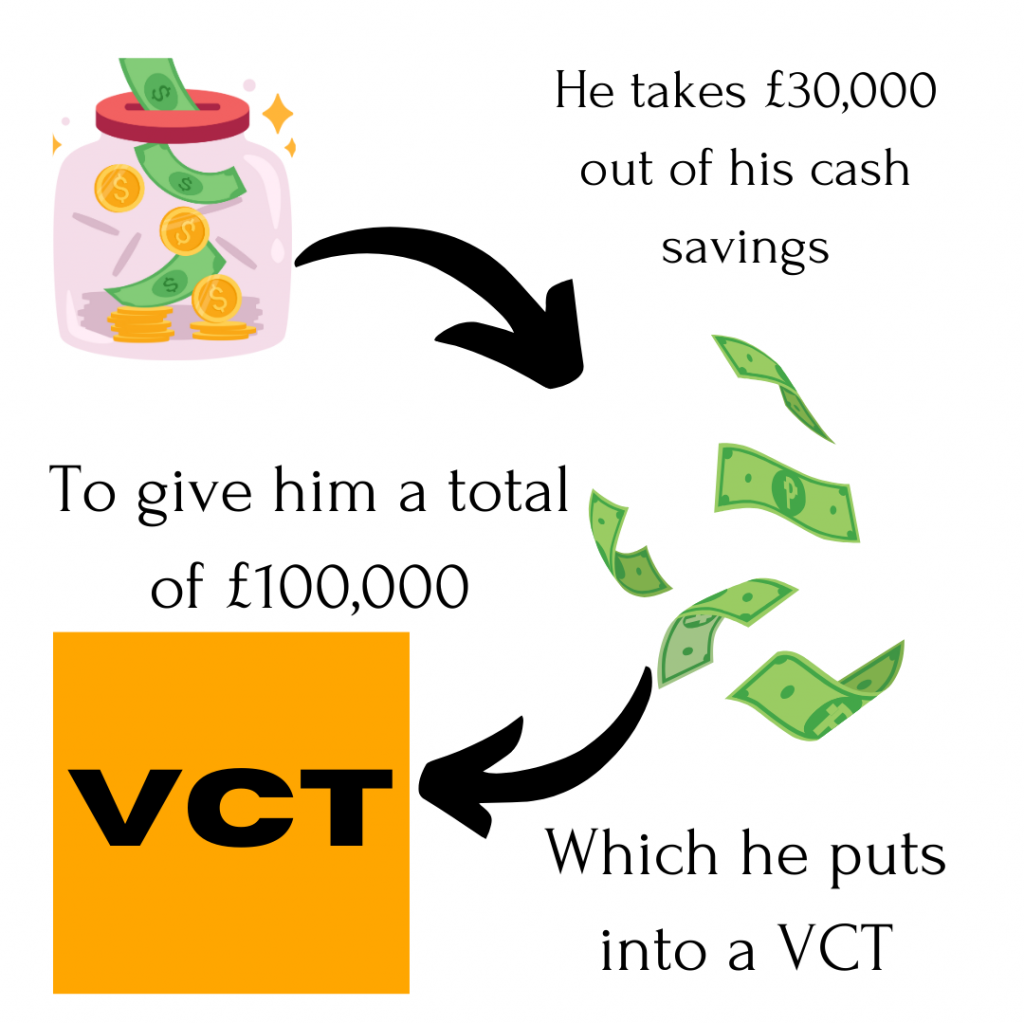

He invests this £100,000 in a VCT, using an extra £30,000 from his cash savings.

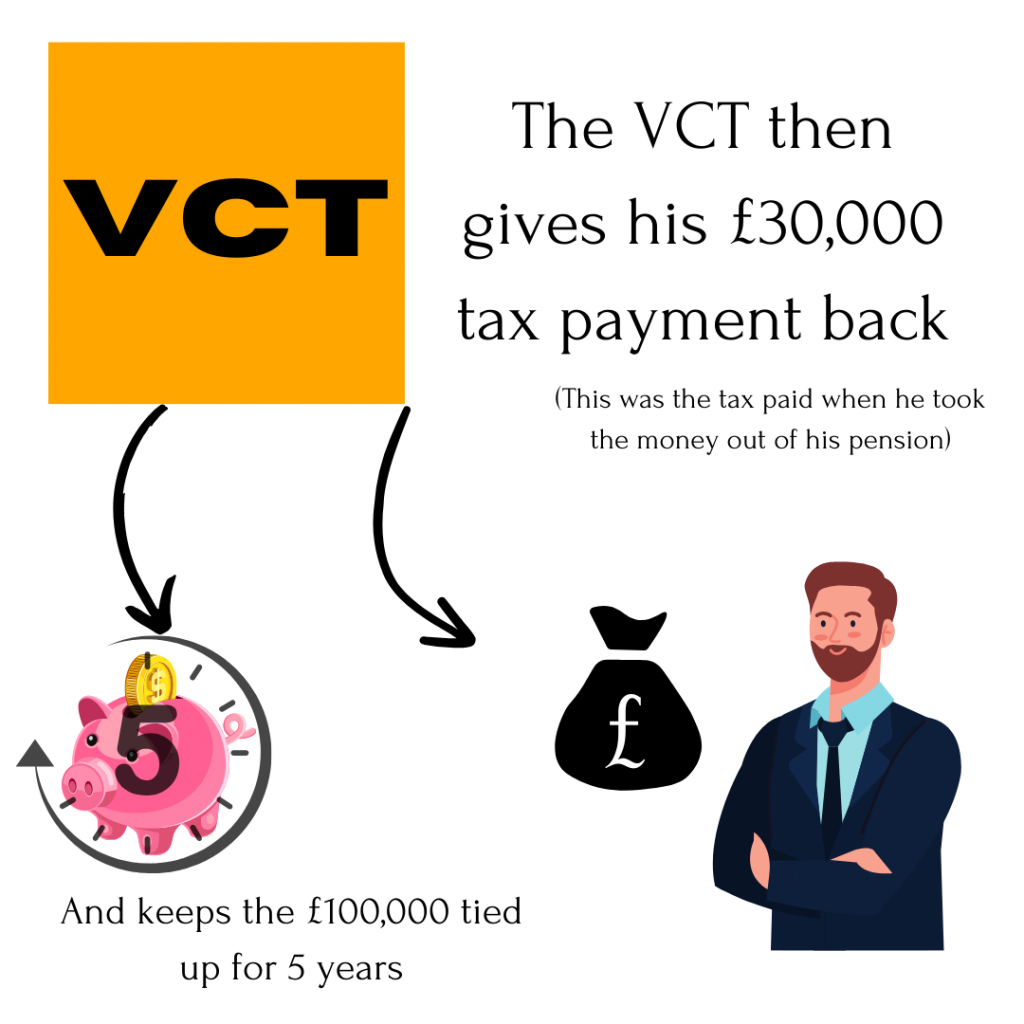

The VCT is a tax reducer, and reduces his income tax by 30p for every £1 contribution.

A contribution of £100,000 means his tax bill is reduced to £0, so he would get back the £30,000 income tax he paid on the pension withdrawal.

So, the £100,000 withdrawal has not cost anything in terms of income tax (provided he keeps the VCT for five years).

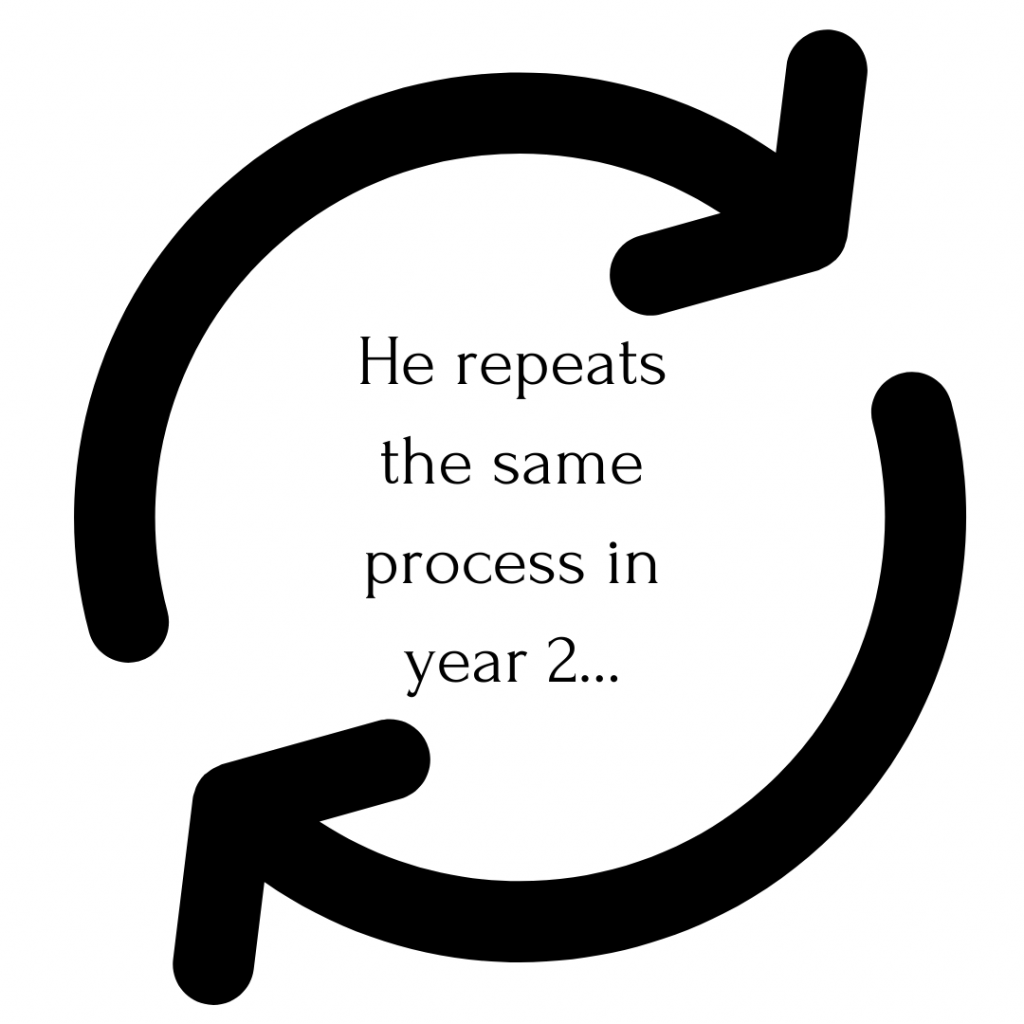

The following year he repeats the process.

Now there has been taken £200,000 out of his pension, and not paid any income tax on it.

If he had not used a VCT, he would have to pay £76,000 in tax, leaving £124,000 after tax.

Five years later, he takes the £200,000 out of the VCT to buy his holiday home

His pension is still available to take to fund his retirement.

It would of course be possible to take out larger amounts, and do this process. It is possible to pay up to £200,000 per year into a VCT, so it would be possible to strip out his pension completely and reinvest it into VCTs over the course of four years. See lifetime tax reducer for more information.

This is a very simplistic example of how it would work. In reality there practicalities to overcome, and timing issues. And in reality a more complex income tax calculation. Nonetheless it is an example how a VCT can be used to take funds from a pension without paying income tax.

This example assumes no growth or return on the VCT, and the fact that it might be bad idea from an inheritance tax point of view to take funds out of the pension. (Although some VCTs are qualify for business property relief, and would escape inheritance tax after two years).

If you have a question about reducing your tax, or want advice, or just want to have a chat about it with a UK Qualified Independent Financial Adviser, then phone now on 01793 686393 or contact us online.